When the number of buyers in the housing market outnumbers the number of homes for sale, it’s called a “seller’s market.” The advantage tips toward the seller as low inventory heats up the competition among those searching for a place to call their own. This can create multiple offer scenarios and bidding wars, making it tough for buyers to land their dream homes – unless they stand out from the crowd. Here are three reasons why pre-approval should be your first step in the homebuying process.

1. Gain a Competitive Advantage

Low inventory, like we have today, means homebuyers need every advantage they can get to make a strong impression and close the deal. One of the best ways to get one step ahead of other buyers is to get pre-approved for a mortgage before you make an offer. For one, it shows the sellers you’re serious about buying a home, which is always a plus in your corner.

2. Accelerate the Homebuying Process

Pre-approval can also speed up the homebuying process, so you can move faster when you’re ready to make an offer. In a competitive arena like we have today, being ready to put your best foot forward when the time comes may be the leg-up you need to cross the finish line first and land the home of your dreams.

3. Know What You Can Borrow and Afford

Here’s the other thing: if you’re pre-approved, you also have a better sense of your budget, what you can afford, and ultimately how much you’re eligible to borrow for your mortgage. This way, you’re less apt to fall in love with a home that may be out of your reach.

Freddie Mac sets out the advantages of pre-approval in the My Home section of their website:

“It’s highly recommended that you work with your lender to get pre-approved before you begin house hunting. Pre-approval will tell you how much home you can afford and can help you move faster, and with greater confidence, in competitive markets.”

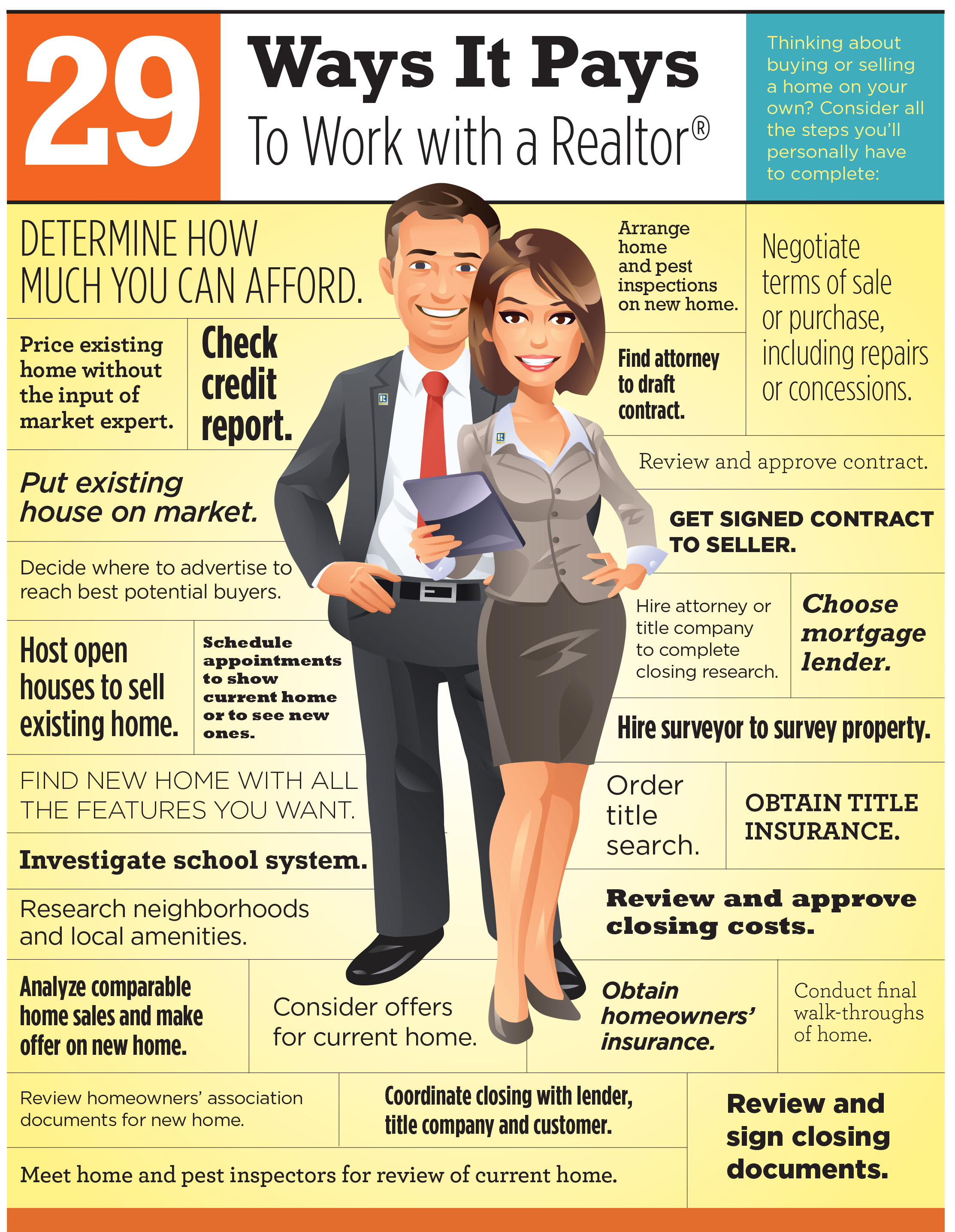

Local real estate professionals also have relationships with lenders who can help you through this process, so partnering with a trusted advisor will be key for that introduction. Once you select a lender, you’ll need to fill out their loan application and provide them with important information regarding “your credit, debt, work history, down payment and residential history.”

Freddie Mac also describes the ‘4 Cs’ that help determine the amount you’ll be qualified to borrow:

- Capacity: Your current and future ability to make your payments

- Capital or Cash Reserves: The money, savings, and investments you have that can be sold quickly for cash

- Collateral: The home, or type of home, that you would like to purchase

- Credit: Your history of paying bills and other debts on time

While there are still many additional steps you’ll need to take in the homebuying process, it’s clear why pre-approval is always the best place to begin. It’s your chance to gain the competitive edge you may need if you’re serious about owning a home.

Bottom Line

Getting started with pre-approval is a great way to begin the homebuying journey. Reach out to a local real estate professional today to make sure you’re on the fastest path to homeownership.