According to many experts, the real estate market is expected to continue growing in 2021, and it’s largely driven by the lasting impact the pandemic is having on our lifestyles. As many of us spend extra time at home, we’re reevaluating what “home” means and what we may need in one going forward.

Here are 4 reasons people are reconsidering where they live and why they’re expecting to buy a home this year.

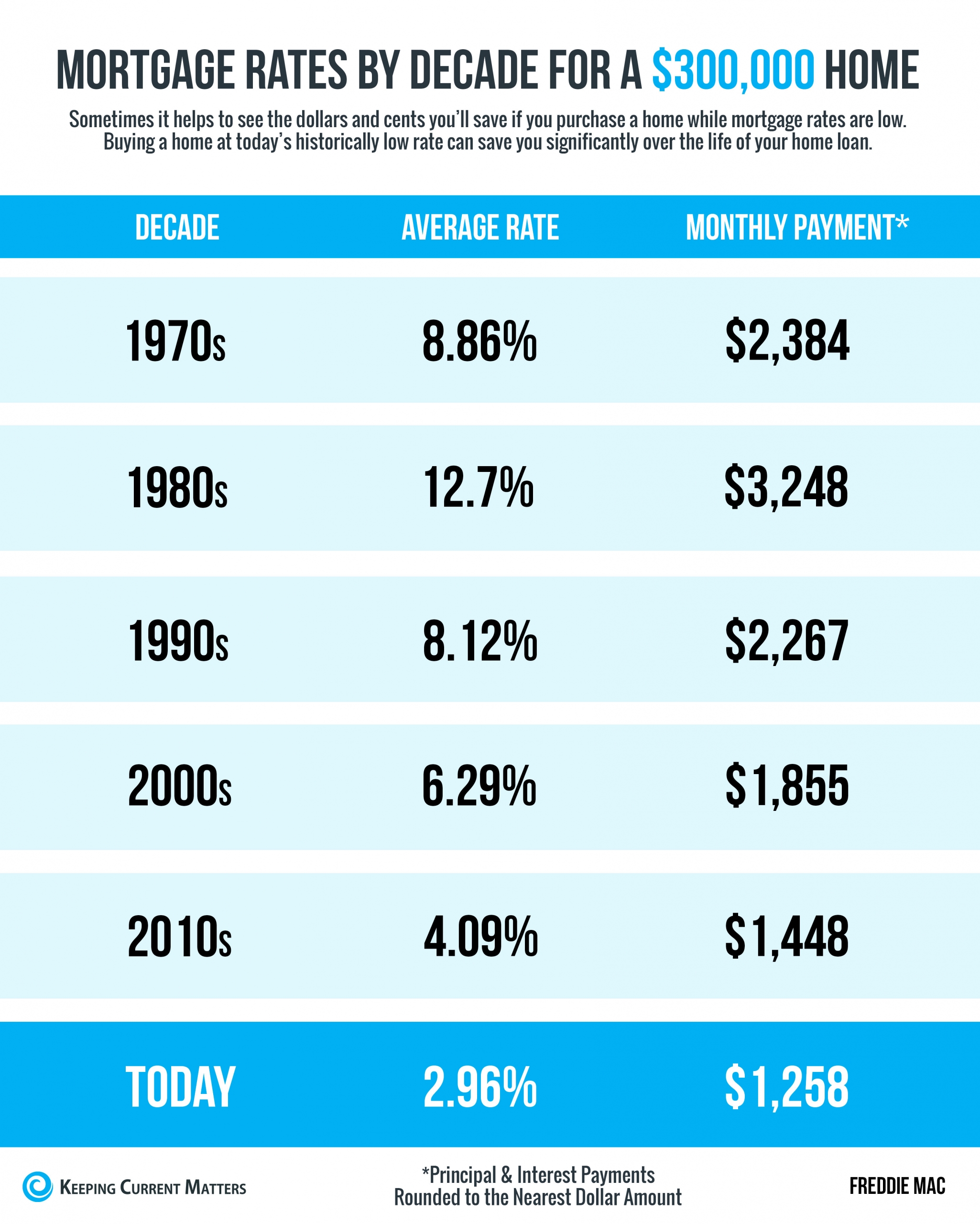

1. Record-Low Mortgage Interest Rates

In 2020, the average interest rate for a 30-year fixed mortgage hit a record low 16 times, continuing to fall further below 3%. According to Freddie Mac, the average 30-year fixed interest rate today is 2.65%. Many wonder how low these rates will go and how long they’ll last. Len Keifer, Deputy Chief Economist for Freddie Mac, advises:

“If you’ve found a home that fits your needs at a price you can afford, it might be better to act now rather than wait for future rate declines that may never come and a future that likely holds very tight inventory.”

This sense of urgency is driving many to buy this year.

2. Working from Home

Remote work is a new normal for many businesses, and it’s lasting longer than most expected. Many in the workforce today are discovering they don’t need to live close to the office anymore and they can get more for their money by moving a little further outside of the city limits. David Mele, President at Homes.com, says:

“The surge in the work-from-home population has rewritten the playbook for many homebuying and rental decisions, from when and where to relocate, to what people are looking for in their next residence.”

The reality is, for some people, working remotely in their current home is challenging, especially when there may be other options available.

3. More Outdoor Space

Another new priority for homeowners is having more usable outdoor space. Being at home is driving those in some areas to seek less densely populated neighborhoods so they have more room to stretch their legs. In addition, those living in apartments and townhomes are often looking for extra square footage, both inside and out.

According to the State of Home Spending report by HomeAdvisor, of the households surveyed, almost half reported spending 27% more on outdoor living over the past year. This is a trend that’s expected to grow in 2021 and beyond.

4. Avoiding Renovations

It’s recently come to light that many homeowners would also rather buy a new home than go through the process of fixing up the one they have. According to the 2020 Profile of Home Buyers and Sellers report from the National Association of Realtors (NAR), 44% of homebuyers purchased a new home to “avoid renovations or problems with the plumbing or electricity.”

Depending on what needs to be addressed, today’s high buyer demand may make it possible to skip some renovations before selling. Many of these homeowners have prioritized buying over renovating for convenience and potential cost savings.

Bottom Line

It’s clear that homeownership needs are changing. As a result, Americans are expected to move in record numbers this year. If you’re trying to decide if now is the right time to buy a home, contact a local real estate professional today to discuss your options.

source